CUBA STANDARD — No matter how sound their business plans are, European investors in Cuba, competing for a $500 million Havana airport project and more than $1 billion worth of renewable-energy projects, are facing an uphill struggle to obtain funding. That’s due to a toxic mix of European banks’ fear of U.S. sanctions and Cuba’s rock-bottom debt rating, which makes any borrowing costly and complicated — if not outright impossible.

CUBA STANDARD — No matter how sound their business plans are, European investors in Cuba, competing for a $500 million Havana airport project and more than $1 billion worth of renewable-energy projects, are facing an uphill struggle to obtain funding. That’s due to a toxic mix of European banks’ fear of U.S. sanctions and Cuba’s rock-bottom debt rating, which makes any borrowing costly and complicated — if not outright impossible.

Although the French government apparently played a key role in getting Cuban authorities to sit down with construction giant Bouygues and Aéroports de Paris to talk about managing and expanding Havana’s José Martí International Airport, as well as building a cargo airport west of Havana, a successful outcome for the French consortium is far from guaranteed, a close observer says.

“It’s based on a simple letter of intent,” a European diplomat who closely follows the project said about the airport talks. “The negotiation is still open to competitors, and the proposals have not been completed.”

The biggest obstacle is funding — specifically, French banks’ reluctance to get involved, according to several observers who declined to go on the record.

“The consortium is still searching for financing, and the project is far from being tied up, because practically all French banks are declaring their fear of Uncle Sam’s big stick,” the diplomat told Cuba Standard. He added that French banks are going “even beyond the letter of OFAC regulations”, referring to the U.S. agency in charge of enforcing financial sanctions.

According to observers, the consortium could use a combination of a debt-to-projects conversion fund the French and Cuban governments are about to set up, and fresh mid-term credit by France’s export guaranty agency or long-term loans from French development agency AFD. But the availability of French government-backed funds for the project apparently makes no difference for the commercial banks.

Cuba, the outcast

Fear of Uncle Sam’s big stick aside, commercial banks also have a long history of treating Cuba as an outcast. Cuba has been serving sovereign debt religiously for the past eight years, recently settled with governments that hold defaulted Cuban debt dating back as far as the 1980s, and Moody’s earlier this year replaced the ‘stable’ with a ‘positive outlook’ for its Caa2 junk rating of Cuban debt. The country, which has been excluded from any international finance institutions, is also making steps towards engaging with multilateral lenders such as CAF-Development Bank of Latin America. But bankers — not surprisingly — want to be on the safe side and take a wait-and-see attitude, continuing — at worst — to charge Cuban borrowers whopping interest rates for any loan longer than one year, or trying to get a hold of revenue streams originating outside of Cuba as guarantee for any loans at best.

Renewable-energy projects in Cuba, even though they may be 100% owned by foreign investors, are not likely to obtain any loans from commercial banks, predicts a European businessman familiar with banks and the island, because the only revenue stream these investors have at their hands is from the Cuban state utility.

“That’s the reality we’re still dealing with in Cuba,” the businessman told Cuba Standard. “That is, unless someone at the top makes the strategic decision to take a risk and lend with a long-term perspective,” he said about banks.

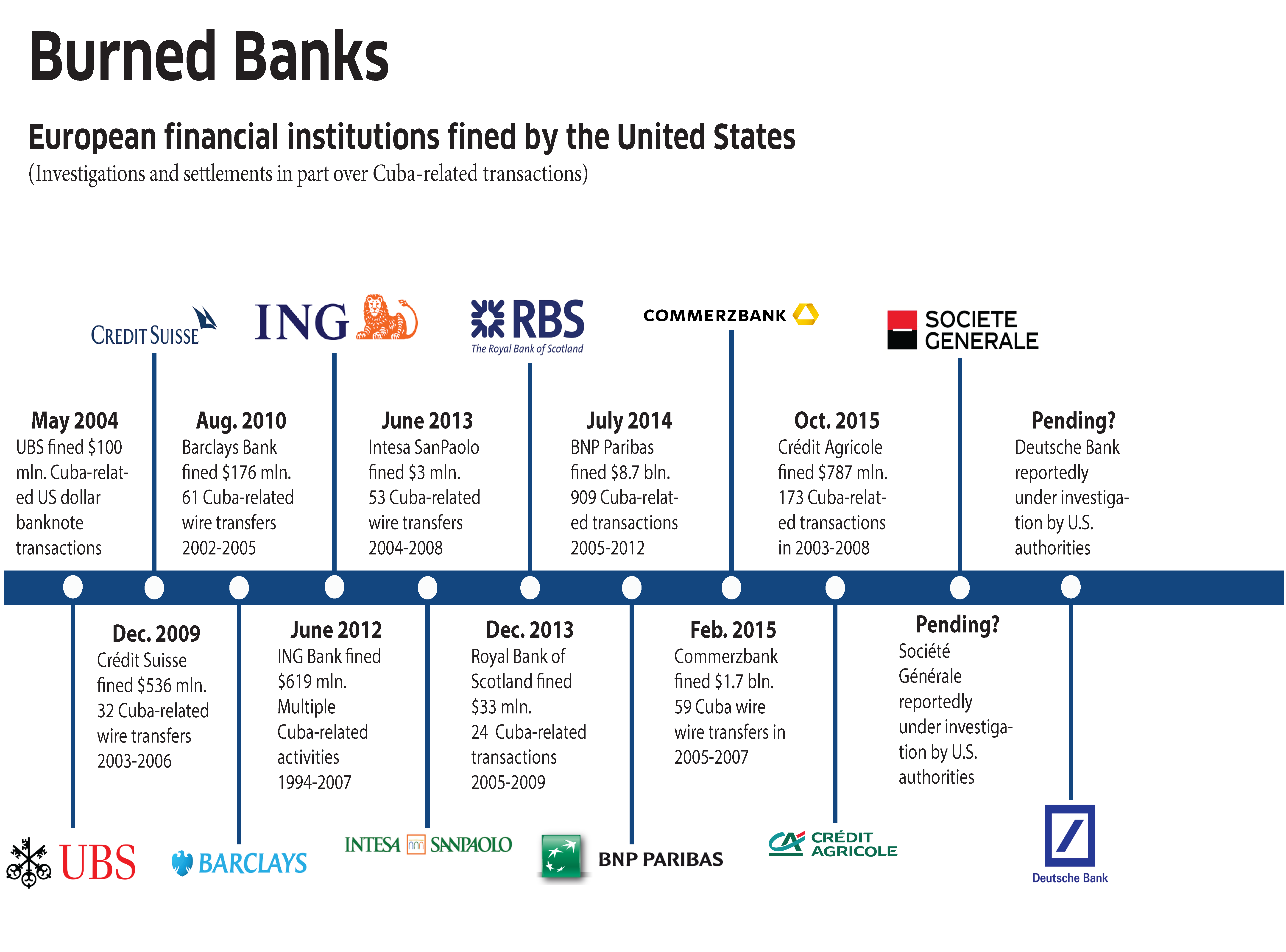

Burned banks

If a €32 billion (revenues) multinational corporation such as Bouygues Bâtiment is having a hard time putting together project finance in Cuba, the challenge is daunting for small, entrepreneurial companies. In the case of a $165 million biomass power project in Villa Clara province, Scottish entrepreneur Andrew Macdonald was forced to take an unusual route to obtain funding — he had to go all the way to Shanghai, and give up control of his startup company, Havana Energy.

If a €32 billion (revenues) multinational corporation such as Bouygues Bâtiment is having a hard time putting together project finance in Cuba, the challenge is daunting for small, entrepreneurial companies. In the case of a $165 million biomass power project in Villa Clara province, Scottish entrepreneur Andrew Macdonald was forced to take an unusual route to obtain funding — he had to go all the way to Shanghai, and give up control of his startup company, Havana Energy.

“Renewable energy and biomass is very much in demand in Europe,” Macdonald said during a recent conference in Havana about investors’ interest. “The returns and potential revenue are fine. The stumbling block is the threat of North American fines.”

Even though the Obama administration recently amended U.S. sanctions regulations, allowing U.S. financial institutions to clear “u-turn” dollar transactions involving Cuban entities and third-country banks, most European financial institutions won’t touch Cuba, according to many sources. Particularly British, French, Swiss and German banks are abstaining from doing any business — no matter whether in US dollars, euros, Swiss francs, or British pounds.

“If you go to any High Street in the UK and ask a UK bank to transfer £10 to Cuba, they tell you they can’t do it,” Macdonald said.

European banks’ abstention is corroborated by Cuban government sources. Cuba’s most recent annual report about the impact of U.S. sanctions, which was released in September, indicates that at least two British banks, as a general policy, refuse any transactions involving Cuba. The report also says that three Italian banks refused to serve an Italian importer of Cuban products; and that two Spanish banks rejected Cuban diplomats and a Spanish company doing business in Cuba as clients.

An old story

The fear of British, French and German banks has its roots in a story that began in the middle of the past century. After World War II, the United States opened a “eurodollar” mechanism under the Marshall Plan to rebuild Europe, leading to wide use of dollars among West European banks in business with third countries, and the development of a separate, less regulated market for the deposit of those funds. But after the Cold War ended, the United States tightened controls and told European banks they now had to route any dollar transfers through U.S. financial institutions.

“The European banks interpreted that as just a technical measure, without realizing that the Americans expected Europeans using U.S. dollars to respect U.S. laws, including their embargos,” a European businessman told Cuba Standard. “That’s why BNP Paribas hid their transactions — naively because they didn’t understand the degree of surveillance new technologies allowed, and naively because they were not aware of the Americans’ propensity to impose their law on the whole world,” he added, referring to the French bank that settled multiple U.S. investigations in 2014 by paying a jaw-dropping fine of $8.9 billion.

The bank’s alleged violations included $1.74 billion of dollar transactions involving Cuba from 2004 to 2010. As part of the settlement, BNP Paribas agreed to stop doing business with Cuba altogether, no matter in what currency.

BNP Paribas was just the most spectacular in a half-dozen enforcement actions against European banks spanning the Obama administration (see graphic on page 2), including after President Barack Obama’s Dec. 17, 2014 normalization announcement. As recently as October 2015 — amid the ongoing U.S.-Cuba normalization process — U.S. federal and state agencies fined France’s Crédit Agricole SA and its investment bank subsidiary CACIB $787 million, in part over Cuba-related dollar transactions. That was preceded in March 2015 by a $710 million settlement with Germany’s Commerzbank; early this year, Commerzbank “communicated to Cuban banks it would cease its operations in the coming months, as a result of the fine imposed by the United States,” the Cuban government said in its annual report about U.S. sanctions.

What’s prompting banks to stay away

If close observers are correct, it is mostly legal insecurity over dollar-transaction skeletons in the banks’ closet that continue to prompt European financial institutions to abstain from Cuba.

“Since the banks understood that the ‘big ears’ have copied it all, they’ve been asking themselves what the U.S. could accuse them of, should they be investigated,” the European diplomat said. “Almost all of them know they’ve made a lot of dollar operations five to 10 years ago. But none of them knows to differentiate those that would fail, and those that would be passable under U.S. sanctions if tested, because the records have been filed without having been analyzed from this angle. The fear of an undetermined sanction is even more effective than that of a precise sanction. All banks — or almost all of them — prefer to abstain even from euro transfers to Cuba, Sudan or Iran, or accepting euro funds from those countries, in order to avoid being visible, to stay out of sight.”

“That’s not courageous, but who said that the banking profession requires courage?”, he added.

Seeking ‘highest-level declarations’

Cuban officials warmly welcomed Washington’s “u-turn” amendment in March — while pointing out continued enforcement against foreign banks and suggesting that more needs to be done.

At a press conference in Havana in March, Foreign Minister Bruno Rodríguez emphasized the importance of the dollar-depenalization measure, but said that for foreign banks to feel legally and politically safe enough to engage with Cuba, OFAC will have to issue “numerous legal clarifications.”

“Without doubt, it concerns a significative aspect of the blockade,” he said about the u-turn amendment. “However, for this measure to be viable, there will have to be political declarations at the highest level of the U.S. government.”

“The banks will have to understand whether this measure, in effect, means that in the near future the financial persecution against Cuba ceases. The intimidating effects accumulated during decades will have to be reverted, particularly in the recent period during which sanctions were applied against international banks — in other words, foreign banks from third countries — for more than $14 billion just for relating in a totally legitimate way with Cuba.”

When asked in the recent past by Cuba Standard, U.S. sanctions officials declined to say whether they stopped Cuba-related enforcement against third-country banks, but hinted that all recent enforcement actions against foreign banks are about transactions that date back to before normalization.

Meanwhile, Obama administration and Cuban officials have held two joint workshops for finance executives this summer — one in Havana and one in New York — offering clarifications of what is and what isn’t possible under new U.S. regulations.

“We’ve issued frequently asked questions and talked at a number of banking workshops, and talked about all the availability and all the great many authorizations we’ve introduced, so that Cuban financial institutions can engage and can offload any surplus of dollars they may have accumulated through different trade,” a senior Obama administration official said in a conference call with reporters in October.

However, all of the clarifications have been aimed at the concerns of Cuban and U.S. banks, according to participants in the workshops, not third-country banks.

What’s more, increasing the insecurity, a new president will be in the White House in January, and his or her day-to-day practice in regards to enforcing U.S. sanctions with third-country banks is yet to be known.

Obama issued a new presidential policy directive (see page 14) that lays out a more cooperative approach for national security policy towards Cuba. But it could be rescinded very quickly by his successor, Cuban officials have pointed out.

Handing control to Chinese partners

In the meantime, most European banks refuse to touch Cuba, and Andrew Macdonald — even though his company features a former UK energy minister as chairman of the board — saw himself forced to seek funding in a country that is less vulnerable to U.S. enforcement actions.

In May, five years after founding Havana Energy Ltd. and three years after forming the BioPower joint venture with Zerus S.A., a subsidiary of state sugar holding Azcuba, the Scottish entrepreneur announced he obtained funding and an Engineering Procurement Construction (EPC) agreement in China. The deal with Shanghai Electric Co. Ltd. allows the joint venture to go ahead with construction of a $165 million biomass power plant connected to the Ciro Redondo sugarmill in Central Cuba. The main financing contracts have been signed with Shanghai Electric, and the process is about to be wrapped up.

“We are in the final stage of finalizing guarantees, and the Banco Nacional de Cuba is about to implement them,” Zerus President Francisco Llaó Martínez said in September.

Macdonald refused to reveal any details about the arrangement with his Chinese partners, citing fears about the U.S. “financial blockade”. He later confirmed to Cuba Standard he sold a majority stake in his company to Chinese partners.

Macdonald said that the Ciro Redondo project is only the first of five similar power plants offered by Cuba to BioPower S.A. In total, the joint venture hopes to build a capacity of 310 mw, at an estimated cost of $825 million.

The design of the power plant at Ciro Redondo will be “quickly” replicated in plants 2,3,4 and 5, Macdonald said. Asked whether Havana Energy will have the capacity to secure enough funding for the additional power projects, he said it does.

“In the absence of banks, there is an opportunity for frontier investors,” said the European businessman familiar with banking in Cuba, asked about the Shanghai Electric deal. “No doubt.”

Spanish, Canadian banks to the rescue?

Short of seeking investors such as Shanghai Electric, or “burned” European banks returning to doing business in Cuba, there may still be an alternative within reach.

Several foreign banking sources in Cuba suggest that Spanish and Canadian banks might be in a position to fill some of the gaps left by their French, British and German competitors. Spain’s Bankia, Banco Sabadell, Santander and BBVA enjoy a more robust presence in Cuba, because they have not been exposed to the eurodollar system, and because they have long been doing considerable business throughout Latin America. Thanks to that, they have been more aware of the limits imposed by the hegemonic power to the North, these sources say.

Similarly, National Bank of Canada, Royal Bank of Canada, and Scotiabank could start with a relatively clean slate vis-a-vis U.S. sanctions enforcers.

“Spanish and Canadian banks have behaved more like Latin banks,” the European businessman said. “They have learned how to deal with the hegemonic power. They have always been very aware to not cross that fine line with U.S. authorities.”

In addition, banks from non-traditional countries, such as National Bank of Qatar — the Persian Gulf region’s largest lender — Panama’s Multibank, and another Latin American bank are in the process of opening representative offices in Cuba.